Why Australian retirees aren't happy and what we can do about it

When it comes to retirement planning, we could be forgiven for giving ourselves a collective pat on the back here in Australia.

Not only are we further down the path of defined contribution (DC) provision than any other major pension market, but our system is lauded as one of the most advanced in the world.

As Robin Bowerman, Principal, Market Strategy & Communications at Vanguard Australia, observes in a recent Smart Investing article, a recent survey ranked Australia as the world's second best country for a comfortable retirement-behind only our neighbours in New Zealand.

So developments here are often seen as a bellwether for other markets as they move further down the DC path and grapple with the challenges of moving pension liabilities off corporate and government balance sheets and placing more responsibility on the shoulders of individuals.

But let’s not get too complacent. Australia's retirement system definitely has some great attributes, but is it leading to satisfactory outcomes for all retirees?

The unhappy country

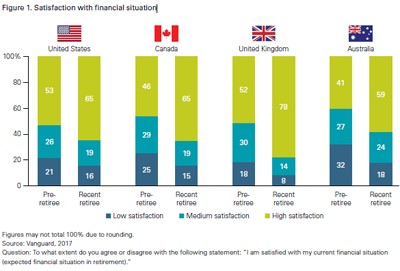

The transition to retirement generally brings increased contentment with uncertainty giving way to acceptance, as you can read in this great piece by my colleague in the US Anna Madamba.

And while this is as true for Australians as it is for American, British and Canadian retirees, the level of local respondents reporting high satisfaction is the lowest of the four countries surveyed in Vanguard's recent paper, Retirement transitions in four countries – as you can see in the graph below.

So why are we so relatively unhappy here in Australia? I'd like to look at the part that choice plays in influencing outcomes.

DC models like ours transfer the primary responsibility for retirement from the government and the employer to the individual. This naturally generates a number of choices for retirees.

- How much should I take as a lump sum and how much as an income stream?

- Should I think about an account-based pension or an annuity...or a combination of both?

- How do I manage my retirement income to maximise my government entitlements?

Compared with some overseas retirement regimes, our combination of compulsory superannuation, means-tested age pension and relatively complex drawdown requirements requires a higher degree of financial literacy and dependence on professional advice.

And while most of us would support the principle of encouraging deeper engagement, in practice the need to choose between more complex options may be leading to dissatisfaction.

Too many flavours?

Behavioural scientists have shown that increased choice does not necessarily lead to increased happiness.

The famous Jam Study demonstrated that the more options we have, the harder it is to make a decision. Faced with more flavours of jam, consumers buy fewer jars. For some this can end in choice paralysis. For others it can lead to the well-documented phenomenon of buyer's remorse as they look back with regret at the jam flavours they didn't buy.

It's the same with super.

- What if I'd taken more advantage of super's concessional tax framework by putting more before-tax contributions into my super while I was working?

- What if I'd put my super into a lower-cost fund that charged less for a similar outcome?

- What if I'd changed my growth/defensive asset mix before making the transition to retirement?

Cutting a path ahead

As an industry we need to cut through the tyranny of choice overload and make sense of retirement planning. We can do this in two main ways.

From a mass customised ‘default’ perspective, product manufacturers can move towards adopting the incoming CIPR (Comprehensive Income Products for Retirement) architecture that will help to develop clearer pathways to retirement.

And from a bespoke advice perspective, financial advisers can play a crucial role in helping clients make sense of the choices and guide them to a satisfactory outcome in retirement.

Based on: Retirement transitions in four countries, January 2017, Anna Madamba, PhD, and Stephen P. Utkus

Paul Murphy

07 July 2017

www.vanguard.com.au

Hot Issues

- ATO encourages trustees to use voluntary disclosure service

- Beware of terminal illness payout time frame

- Capital losses can help reduce NALI

- Investment and economic outlook, August 2024

- What the Reserve Bank’s rates stance means for property borrowers

- How investing regularly can propel your returns

- Super sector in ASIC’s sights

- Most Popular Operating Systems 1999 - 2022

- Our investment and economic outlook, July 2024

- Striking a balance in the new financial year

- The five reasons why the $A is likely to rise further - if recession is avoided

- What super fund members should know when comparing returns

- Insurance inside super has tax advantages

- It’s never too early to start talking about aged care with clients

- Capacity doubts now more common

- Most Gold Medals in Summer Olympic Games (1896-2024)

- SMSF assets reach record levels amid share market rally

- Many Australians have a fear of running out

- How to get into the retirement comfort zone

- NALE bill passed by parliament

- Compliance focus impacts wind-ups

- LRBA interest rates increase for 2025

- Income-free areas set to increase from 1 July

- Most Spoken Languages in the World

- Middle-to-higher incomes boosting SMSF growth

- Investment and economic outlook, May 2024

- Transitioning into retirement: What you should know

- Plan now to take advantage of stage 3 tax cuts

- Deeming freeze a win for Age Pensioners

Article archive

- April - June 2024

- January - March 2024

- October - December 2023

- July - September 2023

- April - June 2023

- January - March 2023

- October - December 2022

- July - September 2022

- April - June 2022

- January - March 2022

- October - December 2021

- July - September 2021

- April - June 2021

- January - March 2021

- October - December 2020

- July - September 2020

- April - June 2020

- January - March 2020

- October - December 2019

- July - September 2019

- April - June 2019

- January - March 2019

- October - December 2018

- July - September 2018

- April - June 2018

- January - March 2018

- October - December 2017

- July - September 2017

- April - June 2017

- January - March 2017

- October - December 2016

- July - September 2016

- April - June 2016

- January - March 2016

- October - December 2015

- July - September 2015

- April - June 2015

- January - March 2015

- October - December 2014

July - September 2017 archive

- ATO to release further guidance on reserves

- A real-world benchmark for SMSF performance

- How is your super going, ready for retirement?

- Our 'hardest' SMSF tasks

- Lack of literacy promotes unrealistic goals

- Young investors: Time is on your side

- Is your SMSF retirement-ready?

- Key Economic Indicators, 2017 - updated

- Investors acting their age

- ATO locks in details, addresses panic on real-time reporting

- Government ‘undermines’ tax system in new moves on property expenses

- Multiple super accounts in a 'gig' society

- Why Australian retirees aren't happy and what we can do about it

- Doing a budget is a good idea but ....

- Technical expert flags estate planning strategies for 2017-18

- Government to shut down salary sacrifice loophole

- Items that heat up your depreciation deductions

- ‘Tens of thousands’ of SMSFs at risk with ECPI

- Do’s and don’ts of estate planning

- LISTO to help boost women’s super

- Smart ways to stretch retirement money

- Low economic growth likely for years

- Recorded Crime - Offenders, 2015-16

- Adequacy of savings still a concern among Australians