What it will take to close the super gap between men and women

There’s a lot of talk about in how to close the super gap between men and women, with women often retiring with far less than men.

The main drivers of this are due to women both earning less and taking time out of the workforce to care for children and other family members.

In a previous column, I discussed steps women and their partners can take to close this gap.

A new report from Women in Super and research firm Rice Warner reinforces the risks that the gender gap poses for women and offers data on the roots of the problem.

Previous research showed that because women have less in super and rely more heavily on the age pension, they are more likely than men to face financial insecurity and poverty in retirement.

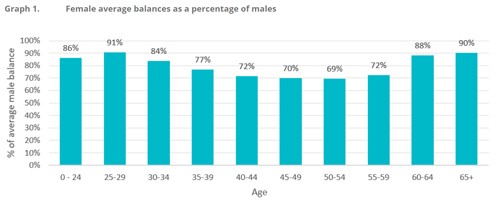

As you can see from the Rice Warner data in the chart below, the super gap starts to widen when women are in their 30s, suggesting that taking time out of the workforce to rear children diminishes income and super contributions.

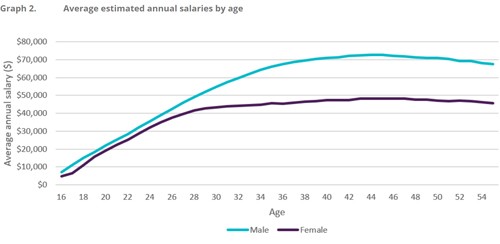

The research also demonstrates that women start out their careers with pay that is close to their male counterparts, only to see a gap emerge as women enter their 20s and 30s. The source of this divergence is not clear, but one likely cause is that women are more likely to leave work to take care of children or family members, missing out on years in the workforce when promotions and pay raises are most likely.

Investment research shows that men tend to invest more aggressively than women, but Rice Warner said this difference did not contribute significantly to the super gap.

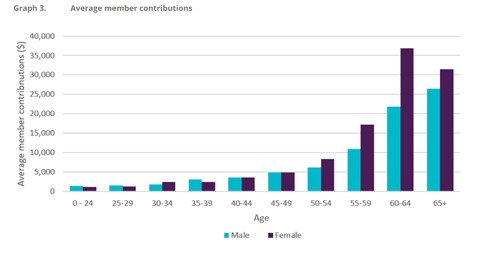

The positive news is that women are taking action to close the gap. They contribute more to super, especially as they approach retirement, which boosts their balances at a crucial stage.

Many women don’t earn enough to make extra contributions, however, and those who do likely can’t compensate enough for years of reduced earnings and super guarantee payments. The roots of the super pay gap are many — gender inequality, the challenges and costs of child care and super policy. Fixing the problem will require changes on all those fronts.

Written by Robin Bowerman

Head of Corporate Affairs at Vanguard.

21 May 2019

vanguardinvestments.com.au

Hot Issues

- ATO encourages trustees to use voluntary disclosure service

- Beware of terminal illness payout time frame

- Capital losses can help reduce NALI

- Investment and economic outlook, August 2024

- What the Reserve Bank’s rates stance means for property borrowers

- How investing regularly can propel your returns

- Super sector in ASIC’s sights

- Most Popular Operating Systems 1999 - 2022

- Our investment and economic outlook, July 2024

- Striking a balance in the new financial year

- The five reasons why the $A is likely to rise further - if recession is avoided

- What super fund members should know when comparing returns

- Insurance inside super has tax advantages

- It’s never too early to start talking about aged care with clients

- Capacity doubts now more common

- Most Gold Medals in Summer Olympic Games (1896-2024)

- SMSF assets reach record levels amid share market rally

- Many Australians have a fear of running out

- How to get into the retirement comfort zone

- NALE bill passed by parliament

- Compliance focus impacts wind-ups

- LRBA interest rates increase for 2025

- Income-free areas set to increase from 1 July

- Most Spoken Languages in the World

- Middle-to-higher incomes boosting SMSF growth

- Investment and economic outlook, May 2024

- Transitioning into retirement: What you should know

- Plan now to take advantage of stage 3 tax cuts

- Deeming freeze a win for Age Pensioners

- Downsizer contributions can be time critical

Article archive

- April - June 2024

- January - March 2024

- October - December 2023

- July - September 2023

- April - June 2023

- January - March 2023

- October - December 2022

- July - September 2022

- April - June 2022

- January - March 2022

- October - December 2021

- July - September 2021

- April - June 2021

- January - March 2021

- October - December 2020

- July - September 2020

- April - June 2020

- January - March 2020

- October - December 2019

- July - September 2019

- April - June 2019

- January - March 2019

- October - December 2018

- July - September 2018

- April - June 2018

- January - March 2018

- October - December 2017

- July - September 2017

- April - June 2017

- January - March 2017

- October - December 2016

- July - September 2016

- April - June 2016

- January - March 2016

- October - December 2015

- July - September 2015

- April - June 2015

- January - March 2015

- October - December 2014

April - June 2019 archive

- Recession on our mind

- What it will take to close the super gap between men and women

- Australia - How are we going as 2018-19 ends?

- LRBAs, guarantees in need of review after property market falls

- Average age for establishing SMSFs sitting at 48.9: Report

- ATO updates valuation guidelines for pension reporting

- ATO figures show jump in starting balances for SMSFs

- Your personal financial register

- Australia’s $4bn Super blackhole impacting self-employed most

- The proper help can be a benefit - age pension

- SMSFs on ATO’s radar in cryptocurrency review

- Limited recourse borrowing arrangements - LRBAs

- What a financial planner does to help.

- Goodbye to ad-hoc portfolios

- Wanted: More voluntary super contributions

- Australia by the numbers – May Update

- Federal Budget 2019 - Overview

- How the 2019 Federal Budget affects you

- The problem with getting to 53 years of age.

- Paying for health care in retirement

- Personal super contributions and the 10% test

- What investors can expect as key moves affecting markets await

- ATO flags PAYG obligations for SMSFs with legacy pensions

- Don't just plan for retirement; Plan for your life

- Consumers misunderstand types of advice

- Budget Time - How's Australia going?